- News

10 May 2011

MOCVD reactor shipments down 18% in Q1 but still up 31% year-on-year

Although first-quarter 2011 installations of metal-organic chemical vapor deposition (MOCVD) reactors were down on fourth-quarter 2010 (ending the seven-quarter streak of sequential growth), the outlook for 2011 remains bright for MOCVD and other upstream equipment and materials suppliers, according to IMS Research’s ‘Quarterly GaN LED Supply and Demand Report’. Global merchant MOCVD reactor shipments fell 18% sequentially to 194 units but this is still up 31% year-on-year, with GaN LEDs the dominant application (with a 97% share).

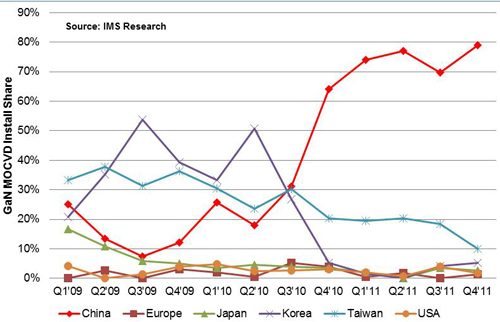

Graphic: GaN MOCVD installations by quarter (Q1/09–Q4/11).

In Q1/2011, Veeco Instruments Inc of Plainview, NY, USA grew its market share of total MOCVD reactor shipments by one percentage point to 44% while maintaining its 44% of the GaN MOCVD market. Aixtron SE of Herzogenrath, Germany maintained its leadership position in both segments, losing a point of market share in total MOCVD shipments from 53% to 52% while maintaining a 53% share of the GaN MOCVD market. Veeco was number one in China and Europe, while Aixtron led in Korea, Taiwan and the USA.

Regionally, China dominated the GaN MOCVD market as expected, accounting for a 74% share (up from Q4/2010’s 64%), while Taiwan maintained a 20% share. Reactors were installed at 23 different companies in China and 9 in Taiwan. In Q1, the top three MOCVD customers globally — and seven of the top 10 — installed tools in China. In particular, China’s San’an Optoelectronics remained the dominant customer for the second consecutive quarter, accounting for more than 20% of tools installed in Q1.

“Looking forward, we are not seeing installations being pushed out in China,” says IMS Research's senior VP Ross Young. “We expected to see some delays, but we have only reduced our 2011 forecast by eight reactors from 1097 to 1089 [still up 36% year-on-year],” he notes. In particular, significant growth is expected in Q2 and Q4, when China’s installations alone are expected to be larger than the entire worldwide 2009 market.

China is the only region expected to show year-on-year growth in installations, rising 181% to 820 tools (75% of the 2011 MOCVD market, up from 36% in 2010). Taiwan is expected to be the number 2 region, with a 16% share (down from 36%, on a modest decline in installations of 14%). Installations in Korea are expected to be down 85%, to 33 tools.

“A number of companies also provided us with their 2012 plans regardless of whether or not there are MOCVD subsidies,” Young continues. “Other incentives and the prospect for rapid growth in LED lighting are proving powerful enough to enable continued investment in LED capacity in China in 2012.”

Young is presenting the latest LED supply and demand information at the SID/IMS Research Green Displays Conference on 18 May at the SID’s Display Week 2011 in Los Angeles.

LED shipments growing 40% to 165bn in 2011

GaN LED market to grow 38% in 2011