- News

6 August 2018

Veeco reports higher-than-expected Q2 profits, despite falling revenue from sales of blue LED MOCVD systems to China

© Semiconductor Today Magazine / Juno PublishiPicture: Disco’s DAL7440 KABRA laser saw.

For second-quarter 2018, epitaxial deposition and process equipment maker Veeco Instruments Inc of Plainview, NY, USA has reported revenue of $157.8m, down slightly on $158.6m last quarter but up 40.6% on $112.2m a year ago.

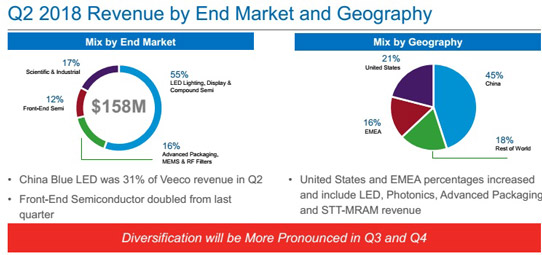

Geographically, the USA has risen from 15% to 21% and Europe, Middle East & Africa (EMEA) from 10% to 16%, while China has fallen from 47% of total revenue to 45% (including sales of metal-organic chemical vapor deposition systems for blue LEDs falling from 39% to 31%) and the rest of the world has fallen from 28% to 18%.

Of total revenue, the Lighting, Display & Compound Semiconductor segment fell slightly from $90m to $88m (from 57% of total revenue to 55%, including the 31% for blue LED MOCVD systems for China).

The Advanced Packaging, MEMS & RF Filter segment - including lithography and Precision Surface Processing (PSP) systems - fell back slightly from $27m to $25m (from 17% of total revenue to 16%).

The Scientific & Industrial segment (including shipments for data storage as well as optical coding applications) fell from $32m to $27m (from 20% of total revenue to 17%).

The Front-End Semiconductor segment (formerly part of the Scientific & Industrial segment, before the May 2017 acquisition of lithography, laser-processing and inspection system maker Ultratech Inc of San Jose, CA, USA) rebounded from $9m to $18m (doubling from 6% of total revenue to 12%), which included revenue from ion beam etch systems for STT-MRAM manufacturing as well as laser spike annealing (LSA) systems.

Ultratech product lines have performed below the projections made at the time of the acquisition, due to lower-than-expected unit volumes of certain vendors’ smartphones that incorporate fan-out wafer-level packaging as well as a delay in the adoption of fan-out wafer-level packaging by other electronics manufacturers. In addition, there has been a delay in the build-out of 28nm fabs in China that were expected to buy LSA systems. Veeco has hence had to assess the carrying value of intangible assets on the books and has recorded an impairment charge of $252m for GAAP results (a non-cash charge, so it does not affect liquidity, day-to-day operations or non-GAAP results). “Relative to the current run rates, we are confident about the growth of this business in future in both the Front-End Semi as well as Advanced Packaging markets,” comments chief financial officer Sam Maheshwari.

“Veeco had solid Q2 performance with non-GAAP gross margin, operating income, net income and EPS at the high end of our guided ranges,” notes chairman & CEO John R. Peeler.

Although gross margin has fallen from 39.1% a year ago and 36.5% last quarter to 35.8%, this exceeds the 33-35% guidance due to better product mix as well as favorable cost structure in warranty and manufacturing areas. Collective first-half gross margin of 36% was also higher than expected.

Operating expenditure (OpEx) has been cut slightly from $46.5m last quarter to $45.7m, better than the guidance of $46-48m. “We continue to make progress towards generating synergies through the integration of Ultratech,” says Peeler. “After unifying our enterprise resource planning (ERP) systems, we’re now eliminating redundant manufacturing operations by closing one of the Singapore manufacturing sites,” he adds. “We expect to complete this initiative by the end of Q1/2019 and anticipate approximately $2m in annualized savings.”

Operating income was $10.8m, down from $11.3m last quarter but up from $6.7m a year ago. Likewise, net income was $7.2m ($0.15 per diluted share), down from $9.2m ($0.20 per diluted share) last quarter but up from $4m ($0.09 per diluted share) a year ago, and towards the high end of the guidance of $1-10m ($0.01-0.20 per diluted share).

However, cash and short-term investments fell during the quarter from $310.6m to $261m, driven by working capital investments. Accounts receivable rose from $108m to $134m due to shipments being backend-loaded in the quarter. Inventory rose from $131m to $146m (from 61 days to 76 days) as Veeco invests to get ready to launch new products in second-half 2018. Lastly, customer deposits fell due to a reduction in orders from China-based MOCVD customers.

Order bookings in Q2 were $132m, down 14.8% on $155m last quarter. This was mainly due to the weakness in the LED Lighting, Display & Compound Semiconductor segment, where Veeco is beginning to see LED makers delay orders as they absorb recently added capacity. Specifically, blue LED MOCVD orders from China for general lighting and backlighting applications fell quarter-over-quarter. “Between 2017 and the first half of 2018, several hundred MOCVD reactors for blue LEDs were shipped into the market and we expect an absorption period,” notes Peeler. In contrast, in Scientific & Industrial markets, Veeco saw a sharp increase in orders from data storage customers, particularly for ion beam deposition tools.

Order backlog fell during Q2 from $331m to $305m. However, about two-thirds of this is scheduled to ship in 2018. The other third includes longer-lead-time ion beam systems that are scheduled to ship in first-half 2019.

“Currently, there are two market dynamics happening at the same time,” notes Peeler. “First, with the addition of Chinese competition for MOCVD, the general lighting and backlighting market is becoming commoditized and pricing has declined. We began to see this towards the end of 2017 with orders at very low gross margins. Second, there is an emergence of new applications such as photonics for 3D sensing, GaN power devices for electronics and electric vehicles, GaN RF devices for 5G RF, and micro-LED displays. Our strategy in this market has been to focus on delivering value through differentiated technology, and our R&D has been aligned with this strategy for some time, resulting in a broad MOCVD product portfolio to address these emerging applications,” he adds.

“We had several announcements throughout the quarter that highlighted the traction we are receiving as a result of our innovation. They highlighted customer wins in our exciting growth markets of Photonics, Display, Advanced Packaging for Memory and Power Electronics,” says Peeler.

“In 3D sensing, we were pleased to see additional phone manufacturers adopt VCSEL-based facial recognition in their devices. We will be shipping systems in the second half of this year to address this demand. We are engaged with several VCSEL manufacturers for their epi process and are getting ready to invest for volume production. We also had recent traction with wet etch and clean products for metal lift-off and photoresist strip for VCSEL manufacturing, and we believe 3D sensing growth is just beginning,” Peeler says. “In GaN RF and GaN Power markets, we are engaged with several large IDMs with our single-wafer Propel platform. Our Propel installed base is expanding and we are well positioned to capitalize when mass production ramps. Recently, we shipped multiple wet etch and clean products to Taiwanese foundries for production of RF amplifiers and other compound semiconductor applications,” he adds. “We expect photonics and RF devices to continue to provide growth potential for us.”

“The overall distribution of bookings across our markets was more balanced, notwithstanding the very strong bookings for Scientific & Industrial,” notes Peeler. Advanced Packaging, MEMS & RF Filters comprised 19% of total bookings, Lighting, Display & Compound Semi 14%, Front-End Semi 21%, and Scientific & Industrial orders 46%. Diversification should be more pronounced in Q3 and Q4/2018.

For third-quarter 2018, Veeco expects revenue to fall to $130-140m, due to the softness in China MOCVD shipments, partially offset by strength in ion beam systems. Gross margin should rise to 36-38%. Despite operating expenses being cut further to $43-45m, the firm expects drops in operating income to $4-9m and net income to $1-6m ($0.03-0.13 per diluted share).

Q4/2018 revenue is seen tracking flat with Q3, but with higher gross margin. While revenue is expected to continue see growth in all four market segments in 2018, low-margin blue LED MOCVD system sales in China in particular are expected to decline. “As sales from the rest of our businesses grow and increase as a proportion of our overall business, we expect gross margin for the company to pick up,” says Peeler. “We remain committed to a target of exiting the year at 40% gross margin [with second-half gross margin improving on first-half 2018’s 36%].”

Beyond Q4, gross margin for calendar 2019 is expected to be higher than 40% as a result of sustainable better product mix and completion of cost-reduction initiatives.

Veeco’s revenue grows 14% in Q1 to $158.6m, driven by MOCVD system shipments to China

Veeco’s revenue rises 9% in Q4/2017, driven by rebound in GaN MOCVD sales to China

Veeco’s Q3 revenue growth driven by continued recovery in MOCVD market

Veeco’s Q2 revenue up 21% year-on-year organically

Veeco completes acquisition of Ultratech for $862m