News: Markets

30 April 2020

Smartphone production falls 10% year-on-year in Q1 and to fall a record 16.5% in Q2

The global COVID-19 pandemic in 2020 has brought about the greatest magnitude of declines in the smartphone market in recent years, according to market research firm TrendForce. Global smartphone production for first-quarter 2020 fell by 10% year-on-year to about 280 million units, the lowest in five years, due to pandemic-induced disruptions across the supply chain, such as delayed work resumption and labor/material shortages, which caused low factory capacity utilization rates.

There are now improvements to both the supply chain and the work resumption statuses of manufacturing and assembly lines, but the pandemic is now making its effects felt on the demand side of the smartphone market by tanking major economies worldwide. Global production for Q2/2020 is forecasted to see a year-on-year drop of 16.5% to 287 million units, the largest decline on record for a given quarter. TrendForce forecasts total annual production of 1.24 billion units, an 11.3% decrease year-on-year.

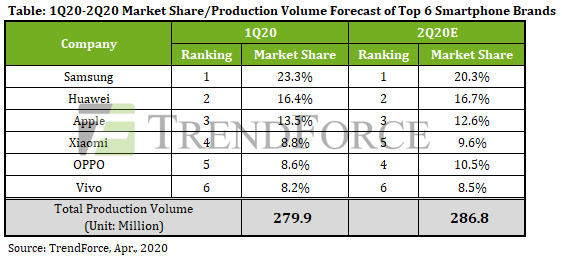

Vivo the only brand among top six showing growth in Q1

Q1/2020 leader Samsung will experience constrained growth this year even without the emergence of COVID-19, says TrendForce. In addition to the market saturation, Chinese brands are exerting continuous pressure on Samsung’s presence in the Southeast Asian and Indian markets by the day. Most of Samsung’s smartphone assembly lines are located in Vietnam and India, and the firm has only about 2% of the market share for smartphones in China. Its production was thus not significantly affected by issues related to the disease during the initial phase of the outbreak in China. Nevertheless, the rapid spread of the disease across North America and Europe in the later part of Q1/2020 compelled Samsung to lower its device output even as its factories were running as usual. The brand’s production volume for Q1 was 65.3 million units, down 9.9% year-on-year. India’s smartphone assembly lines have been suspended since late March due to the imposition of a national lockdown. Furthermore, the global economy has gone into a recession. Samsung’s smartphone production for Q2/2020 will hence fall by 10.7% quarter-to-quarter to 58.3 million units, estimates TrendForce.

Ranked second by production volume in Q1/2020, Huawei was able to have its device assembly lines resume work soon after the Lunar New Year holiday. This brand has seen a steep decline in overseas sales due to its new devices being excluded from Google Mobile Services. Nevertheless, demand from China (its primary market) has started to recover. With the support of domestic demand, Huawei’s smartphone production for Q1/2020 came to 46 million units, in line with TrendForce’s earlier projection. If China’s economy continues to improve, Huawei’s production for Q2 may register quarter-on-quarter growth to about 48 million units. Huawei is sticking with its plan of making a push for its 5G smartphones this year, but 4G models will still account for most of its first-half 2020 smartphone output, and Huawei is also holding a significant inventory of 4G models. So, Huawei’s greatest challenge at present is to simultaneously develop an effective campaign to promote the latest 5G smartphones and sell off the existing stock of 4G smartphones.

Prior to the onset of COVID-19, TrendForce had originally expected Apple to once again reach annual production of 200 million units, due to the release of five new models this year and the phasing out of the popular iPhone 6s series by the seasonal smartphone replacement cycle. However, Apple fell victim to the influence of the coronavirus pandemic, resulting in reduced production of its iPhone lineups this year. In Q1/2020, iPhone production fell by 8.7% year-on-year to 37.9 million units, due to labor and material shortages following the post-Lunar New Year work resumption, in turn ranking Apple in third place. As the firm releases the new iPhone SE with a consumer-friendly price tag in Q2, quarterly iPhone production is expected to stay relatively close to Q1 figures, reaching 36 million units. Apple is still planning to release four new 5G handsets in second-half 2020, but whether the pandemic’s influence will weaken the demand for iPhones going forward remains a noteworthy concern, since iPhones sell at a relatively high retail price, and the iPhone’s primary sales regions are the European and US markets, which are in the midst of dealing with COVID-19.

For fourth-ranked Xiaomi, overseas markets account for over 70% of its sales. As these markets were unaffected by the Lunar New Year, Xiaomi rapidly expanded its production capacity, following its domestic work resumption, to meet demand from overseas channels. But Xiaomi also had to contend with industry-wide issues of labor and material shortages, resulting in lower-than-expected capacity utilization of its production lines. The firm registered Q1/2020 production of 24.5 million units, flat with Q1/2019. TrendForce expects the Q2/2020 acceleration of COVID-19 in India and Indonesia, both of which are major sales regions for Xiaomi, to impact their quarterly smartphone demand and lead to a 10.7% decrease year-on-year in Xiaomi’s Q2 production, to 27.5 million units. The pandemic is projected to have a greater impact on Xiaomi relative to other Chinese brands that rely primarily on domestic sales. In response, Xiaomi will aim to gain a competitive advantage by pricing its 5G handsets for low gross margins, in an effort to capture a greater share of the Chinese market, in turn making up for the shortfall in overseas sales.

OPPO (including OnePlus, OPPO, and Realme) and Vivo, ranked fifth and sixth respectively, benefitted from increased overseas orders, but their capacity utilization rates have been sluggish following post-Lunar New Year work resumption. OPPO posted Q1 production volume of 24 million units, a 10.4% drop year-on-year. On the other hand, Vivo had traditionally maintained conservative production plans during past first quarters, meaning the base period for year-on-year comparisons with Q1/2020 is relatively low. Vivo’s production volume in Q1/2020 grew by 5.5% year-on-year to 23 million units, making it the only smartphone brand in the top six exhibiting year-on-year growth, against the overall trend of declines. TrendForce has lowered its production forecast for Q2 in light of national lockdowns in Southeast Asia and India starting in March: 30 million and 24.5 million units for OPPO and Vivo, respectively, with each brand seeing year-on-year declines of more than 14%.

Annual 5G smartphone production to reach 200 million, depending on Chinese market

The pandemic’s impact prompted governments to prioritize disease prevention and stabilization. Furthermore, consumers generally have a speculative attitude towards purchasing 5G handsets. These two factors diminished the smartphone market’s momentum of transitioning from 4G into 5G in first-half 2020.

In second-half 2020, if the Chinese government stays the course in commercializing 5G and mid-range 5G chips are successfully supplied to the market, the Chinese smartphone market will then see increased incentive to transition into 5G, while also resulting in consumer-friendly retail prices for 5G handsets.

At the moment, as brands fight over 5G market shares, the forecasted annual 5G smartphone production volume remains about 200 million units, with a 16% penetration rate into the overall smartphone market. In particular, Chinese brands have over 60% of 5G smartphone market share, with the domestic Chinese market as their primary sales region. This means that the penetration rate of 5G handsets into the overall smartphone market will depend heavily on feedback from the Chinese market. However, the penetration rate of 5G smartphones does not absolutely reflect the availability of 5G networks, which will depend on the construction of 5G base stations.

Q1/2020 smartphone production forecast cut again, from 12% down to 13.3% down year-on-year