News: Markets

4 January 2021

GaN for fast chargers joining SiC in power electronics market, as 5G infrastructure drives GaN RF

Market research and strategy consulting company Yole Développement says that its ‘Compound Semiconductor Quarterly Market Monitor’ on silicon carbide (SiC) and gallium nitride (GaN) applications evolved in fourth-quarter 2020 to incorporate two new modules:

• Module I: GaN and SiC for power electronics applications; and

• Module II: GaAs and GaN for RF electronics applications.

The firm lists the market dynamics for the sectors as follows.

Power electronics:

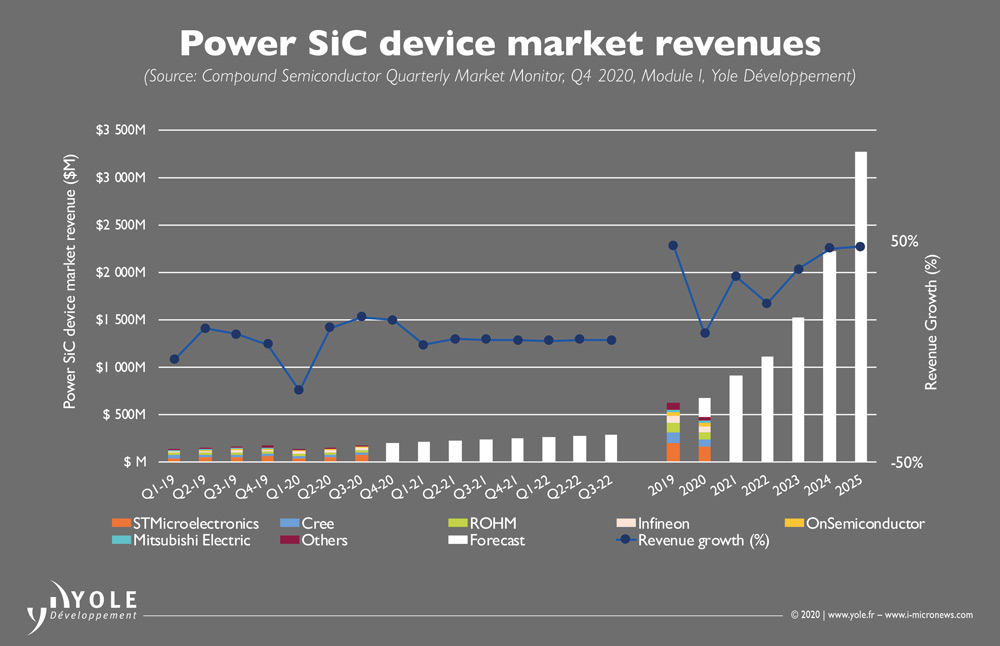

• Power SiC - Despite the short-term impact as a result of the COVID-19 pandemic, SiC device market revenue continues to grow and is expected to exceed $3bn by 2025. Electric vehicles and hybrid electric vehicles (EVs/HEVs) still represent the killer application for SiC devices. Despite the global slowdown in first-half 2020 due to the COVID-19 outbreak, design wins for SiC solutions have recently multiplied, with a bright market outlook for 2019-2020 period, reckons Yole.

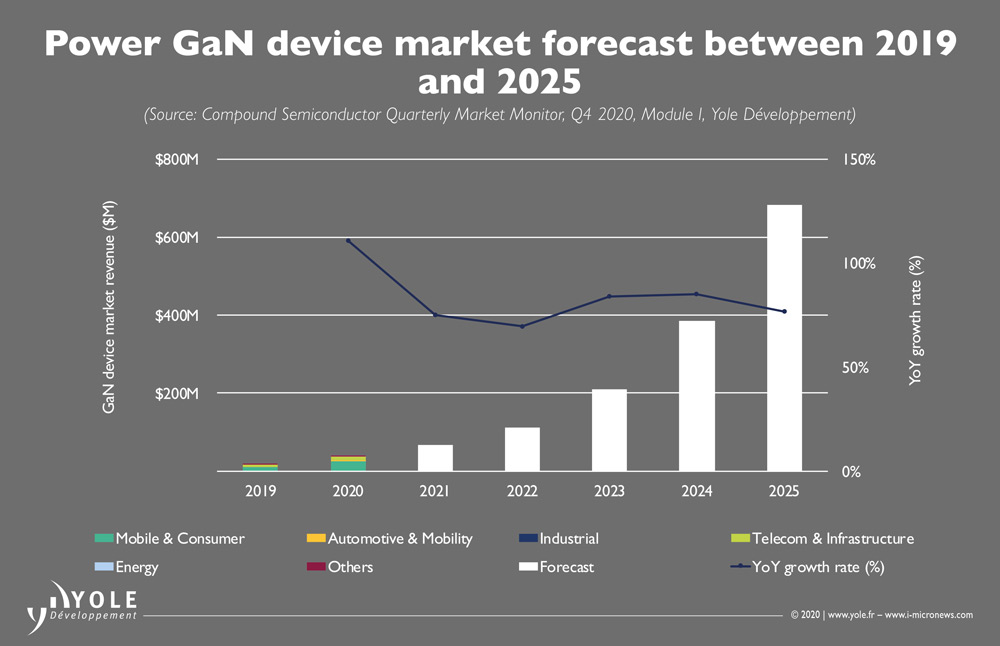

• Power GaN - Yole projects that GaN business will exceed $680m in 2025. The adoption of GaN high-electron-mobility transistors (HEMTs) for Oppo’s in-box fast charger at the end of 2019 boosted the penetration of this wide-bandgap material. Yet GaN has just begun its inroads into the end-consumer mass market, where it will reach volume production, says Yole.

RF:

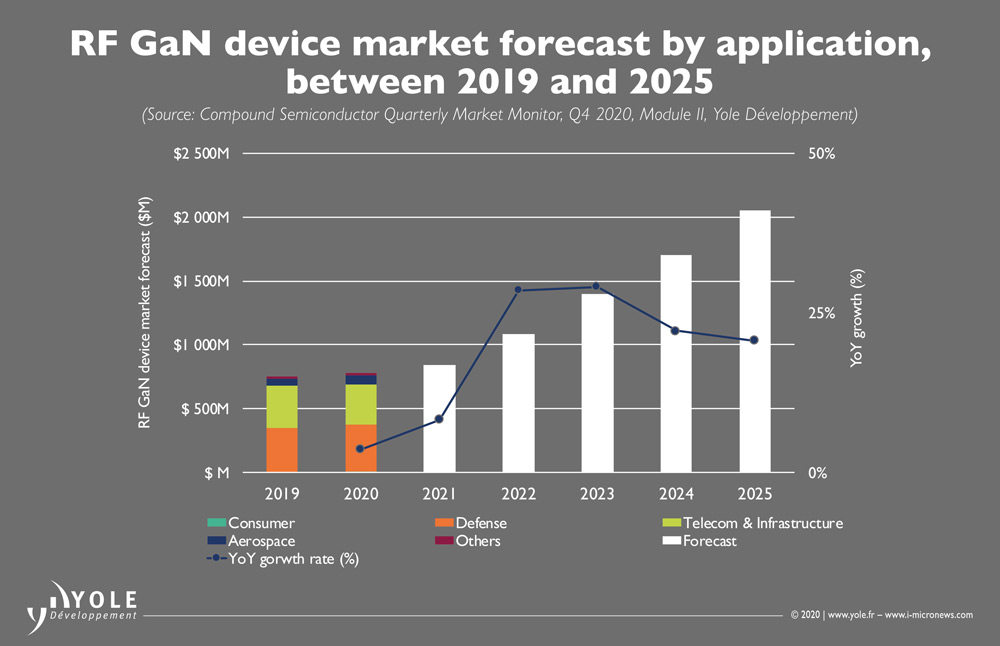

• GaN RF - Yole estimates that the GaN RF device market is rising at a compound annual growth rate (CAGR) of 12% from 2019 to beyond $2bn in 2025. This will be driven by telecom and defense applications, but GaN RF devices for military use are expected to grow rapidly, to more than $1bn by 2025. However, GaN RF business is dependent not only on OEM technology choices but also on the geopolitical context.

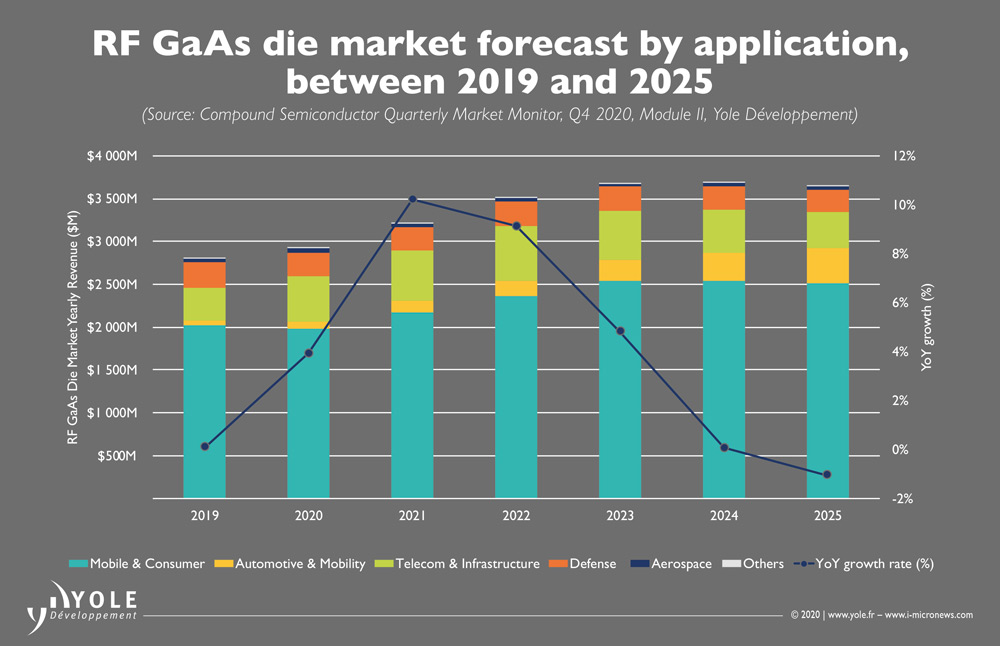

• GaAs RF - The market for RF GaAs die is rise from about $2.8bn in 2019 to over $3.6bn in 2025, driven by the rise of 5G and Wi-Fi 6 demand for handset applications, reckons Yole.

5G telecom infrastructure: GaN’s ascendancy

“In the dynamic 5G infrastructure market, there is a continuous race for more efficient antenna types,” notes Ahmed Ben Slimane PhD, technology & market analyst Compound Semiconductor Monitors, at Yole. “Switching technology from RRH [remote radio head] to AAS [active antenna system] will transform the RF front ends from a low number of high-power RF lines to a large number of low-power RF lines.”

Meanwhile, deployment of higher frequencies in the sub-6GHz and millimeter(mm)-wave regimes is pushing OEMs to look for new antenna technology platforms with larger bandwidth, higher efficiency and better thermal management. In this context, GaN technology has become a serious competitor to silicon-based LDMOS and GaAs in RF power applications, showing continuous performance and reliability improvement, potentially leading to lower cost at the system level. Following its penetration into the 4G LTE telecom infrastructure market, GaN-on-SiC is expected to maintain its strong position in 5G sub-6GHz RRH implementations. However, in the emerging segment of 5G sub-6GHz AAS - massive MIMO deployments - the rivalry between GaN and LDMOS continues. While cost-efficient LDMOS technology carries on with noteworthy progress in high-frequency performance for sub-6GHz, GaN-on-SiC offers remarkable bandwidth, power-added efficiency (PAE) and power output.

GaAs, a key segment

The handset market is the big driver for GaAs devices, with power amplifier (PA) content increasing per phone. In general, 4G LTE cellular phones need to span multiple frequency bands, with an increasing number of PAs per phone. The 5G demand for PAs is at least a factor of two more than for 4G. Adding to that, the stringent requirements for linearity and power make GaAs the material of choice for PAs in the RF front-end module (FEM). Even though CMOS has lower cost per chip, it will not necessarily have the advantage over GaAs when it comes to modules and performance.

“For mobile connectivity, Wi-Fi 6 began to enter the market in 2019,” says Poshun Chiu, technology & market analyst, Compound Semiconductors & Emerging Materials. “Some OEMs launched new phones with Wi-Fi 6: Samsung’s Galaxy S10 in Q1/2019, Apple’s iPhone 11 in Q3/2019, and in Q1/2020 Xiaomi was the first Chinese handset company to have Wi-Fi 6,” he adds. “GaAs solutions are becoming of great interest owing to their linearity and high power output, compared to traditional solutions,” he adds.

Prosperity of power SiC devices due to automotive applications

Since the first commercialization of SiC diodes, the power SiC device market has been driven by power supply applications. Nevertheless, the automotive segment is becoming the killer application, following SiC’s notable adoption for Tesla’s main inverters in 2018. Since then, announcements of SiC solution design wins from different car-makers have multiplied. In 2020, BYD also adopted an SiC-based main inverter solution for its premium models. Other carmakers, such as Audi, Volkswagen, and Hyundai are expected to adopt SiC in their next generation models. In the prospering SiC power market, the automotive segment is undoubtedly the foremost driver, and will hence hold more than 60% of total device market share in 2025.

“However, following the global COVID-19 outbreak, almost all automotive OEMs had to shut down and the supply chain faced significant disruption,” notes Ezgi Dogmus PhD. team lead analyst, Compound Semiconductors, at Yole. “In this context, we expect the power SiC market’s year-on-year (Y-o-Y) growth to slow down to 7% in 2020, with a significant impact in Q1/2020 and Q2/2020,” he concludes.