News: Markets

16 November 2022

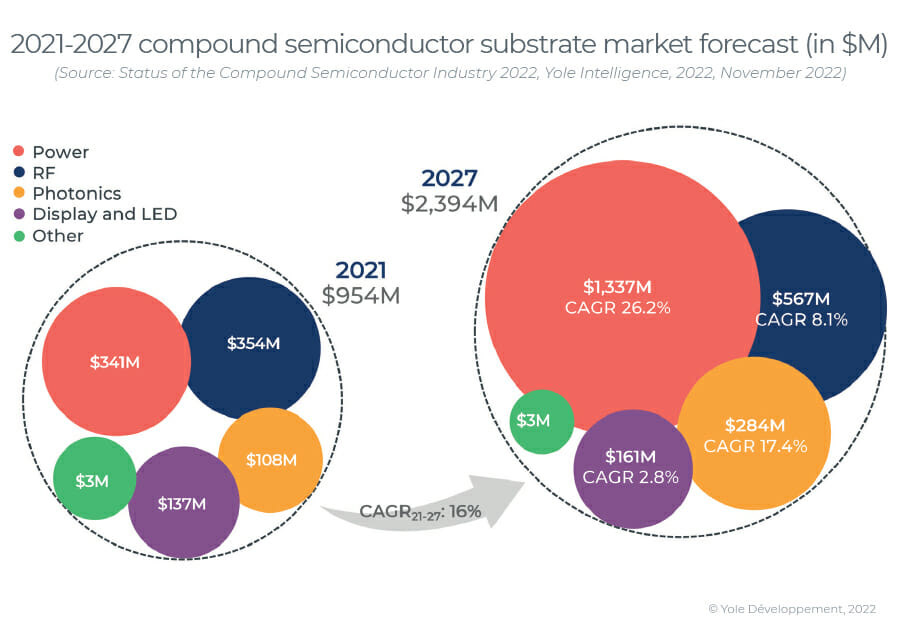

Compound semi substrate market growing at 16% CAGR to $2.4bn by 2027

Driven by power and photonics applications, the compound semiconductor (CS) substrate market is rising at a compound annual growth rate (CAGR) of 16% to nearly US$2.4bn by 2027, according to the report ‘Status of the Compound Semiconductor Industry 2022’ from Yole Intelligence (part of Yole Group).

Compound semiconductors have been adopted in various applications over the past decades. Recently, however, silicon carbide (SiC) and gallium nitride (GaN) in power, GaN and gallium arsenide (GaAs) in radio frequency (RF), GaAs and indium phosphide (InP) in photonics, and LEDs and micro-LEDs in displays have all gained momentum. As a result, the substrate and epiwafer markets are also expected to grow.

“Wolfspeed is the leading SiC substrate and epiwafer supplier for power SiC and RF GaN,” notes Poshun Chiu, senior technology & market analyst specializing in Compound Semiconductors and Emerging Substrates at Yole Intelligence. “As the larger-format substrate is the strategic resource in the next generation of device manufacturing, the opening of 8” wafer fabs and the expansion of material capacity illustrates the ambitious targets aimed at in the coming decade.”

Meanwhile, II-VI closed its acquisition of Coherent and renamed itself, illustrating its change of focus. Now, Coherent is the leading photonic device player as well as the leading SiC substrate supplier for power and RF applications. Moreover, it is working with SEDI (Sumitomo Electric Devices Inc) on RF GaN device manufacturing and has entered the power SiC device business with GE. Both are strengthening their competitiveness from the substrate level to the device level.

AXT, Sumitomo Electric, Freiberger, and SICC are the leading suppliers of GaAs, InP and semi-insulating SiC substrates. Their objectives of growing their revenues rely on expanding into other compound semiconductor materials. Players are looking at the synergy between GaAs and InP substrates for RF, photonic and micro-LED applications. Also, players from semi-insulating SiC are entering n-type SiC, as it is a market with a higher growth rate.

“Epiwafer suppliers benefit from the different dynamics of the compound semiconductor open epiwafer market,” notes Taha Ayari Ph.D., technology & market analyst, Compound Semiconductor and Emerging Substrates, at Yole Intelligence. “IQE has been involved in various compound semiconductor markets (for example, RF GaAs and GaN), as the double-digit CAGRs of InP and GaAs photonics represent markets with both volume and scale. And micro-LED is a booming market, expected to double every year in the coming five years. VPEC has succeeded in becoming the largest supplier of RF GaAs epiwafer in the open market, and the company continues increasing its engagement in photonics for future growth”.

“With LEDs, handset power amplifiers and telecom & datacom, compound semiconductor went through its first inflection point with GaAs and InP in the 1990s,” says Ezgi Dogmus Ph.D., team lead analyst in Compound Semiconductor & Emerging Substrates activity, Yole Intelligence.

As demand for 5G connectivity, electric vehicles (EVs) and fast chargers for smartphones comes to the market, compound semiconductors will grow in both volume and market value, notes Yole. Looking into the future, e-mobility, including higher-voltage applications, sensing in various end-systems, the transition from 5G to 6G, and micro-LED displays will bring inflection points for different compound semiconductor materials, along with more emerging substrates and new applications to come.

www.yolegroup.com/product/report/status-of-the-compound-semiconductor-industry-