News: Markets

10 August 2023

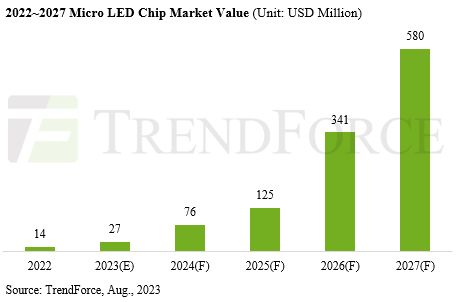

Micro-LED chip market to almost double to $27m in 2023, driven by large displays and wearables

Driven by the mass production of large displays and wearable devices, the micro-LED chip market will grow by 92% year-on-year from $14m in 2022 to $27m in 2023, while rising at a compound annual growth rate (CAGR) of about 136% between 2022 and 2027 to $580m due to the scaling of existing application shipments and the introduction of new applications, forecasts market research firm TrendForce.

Alongside the consistent growth in chip values, ancillary industries — such as transfer and testing equipment, glass and CMOS backplanes, and both active- and passive-matrix drive ICs — are poised for synchronous expansion, adds the firm.

This year, Samsung has unveiled an 89-inch 4K display and plans to further take advantage of the seamless splicing of micro-LEDs by introducing 101-inch and 114-inch models. South Korean brand LG Electronics is set to begin mass production of its 136-inch 4K model, utilizing a larger 22.3-inch backplane and cost-effective 16 µm x 27µm chips, by the end of 2023.

Leading panel maker BOE has taken a similar trajectory, with launches aimed at bolstering growth of the overall industry. The firm launched its P0.9 active-matrix display in second-quarter 2023 and plans to release the P0.51 active-matrix display in fourth-quarter 2023. Additionally, BOE intends to introduce a turnkey solution in 2024. For brands interested in micro-LEDs, this not only diversified production acquisition channels but also contributes to the accelerated development of the overall industry.

Wearables are a key application for micro-LED this year. Pivoting from its traditional LCD operations, AUO has produced the world’s first 1.39-inch micro-LED watch panel. In addition to initially providing it to European luxury watch maker Tag Heuer, other major companies specializing in sports wearables and Japanese watch brands are all potential adopters of micro-LED wearable devices in the future, says TrendForce.

Apple’s rollout of a 2.12-inch micro-LED display for the Apple Watch has been deferred from 2025 to 2026 due to supply chain adjustments. However, production operations for the micro-LED variant are already in motion, signifying possible integration into Apple’s broader product range, including headsets, smartphones and automotive applications.

Booming development in recent years has provided growth opportunities for innovative automotive displays like micro-LEDs. However, due to the prolonged verification processes inherent to the auto sector, tangible mass production of micro-LED displays for vehicles might only materialize post-2026. TrendForce believes that instrument displays with high demand for reliability and brightness, technically advanced head-up displays (HUD), and transparent displays with numerous connections to autonomous driving technology are all primary avenues for micro-LED displays to enter the automotive sector. Auto-makers from Europe, the USA and Japan are showing considerable enthusiasm toward adopting micro-LED techology.

Micro-LED displays continue to compete with technologies like LCOS (liquid-crystal on silicon), micro-OLED (organic light-emitting diode) and LBS (laser beam scanning) when it comes to augmented reality (AR) headsets. Industry leaders like Meta, Google and MIT continue to assess and assist in R&D on micro-LEDs for micro-projection displays, attracted by its balanced performance in terms of brightness, energy consumption, pixel density and light engine size.

On 5 September (9:30-17:00) at the NTUH International Convention Center in Taipei, Taiwan, TrendForce is hosting the ‘Micro-LED Forum 2023’, featuring senior research VP Eric Chiou, alongside industry representatives from Mojo Vision, ITRI, Lumus, Unikorn Semiconductor, Porotech, Nitride Semiconductor, Tohoku University, Coherent, InZiv, AUO and Tianma sharing developments in micro-LED technology and its manifold applications.