News: Markets

14 March 2025

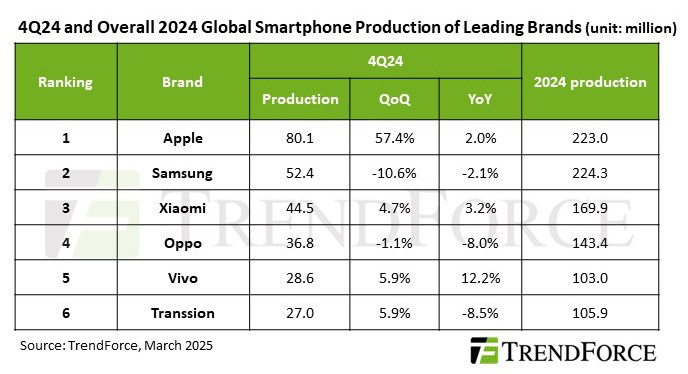

Smartphone production grows 9.2% in Q4/2024 to 334.5 million units

Market research firm TrendForce reports that global smartphone production grew 9.2% quarter-to-quarter to 334.5 million units in fourth-quarter 2024, driven by Apple’s peak production season and consumer subsidies from local Chinese governments. While Apple expanded production with the launch of new models, Samsung faced production declines due to intensified competition in emerging markets.

In first-half 2024, the smartphone market was no longer impacted by high channel inventory compared with the same period the prior year. With seasonal demand and government subsidies driving growth in second-half 2024, total annual production grew 4.9% year-on-year to 1.224 billion units. However, 2025 production growth is expected to slow to just 1.5%, as global economic recovery remains sluggish and geopolitical risks, including tariff hikes, weigh on consumer spending.

Apple surged to the top spot after growing 57.4% quarter-on-quarter to 80.1 million units in Q4/2024. Its total 2024 production remained steady at 223 million units, similar to the previous year. However, its AI-powered features currently support only limited languages, failing to significantly boost sales. A global rollout of multi-lingual AI functions in April is expected to drive renewed demand.

Samsung dropped to second place, falling by 10.6% quarter-on-quarter to 52.4 million smartphones. Its decline in market share reflected the completion of flagship model restocking and increased competition from Chinese brands in key markets like India and Africa. Samsung’s total production in 2024 fell 2.1% year-on-year to 224.3 million units.

Xiaomi (including Redmi and Poco) secured third place, with Q4/2024 production rising 4.7% quarter-to-quarter to 44.5 million units. Full-year 2024 production rose by 15.3% year-on-year to 169.9 million units. Xiaomi’s well-balanced lineup across premium, mid-range and budget segments, coupled with its high-value pricing strategy, resonated with consumers amid economic uncertainty. China’s subsidy programs further boosted its local market share, positioning Xiaomi for continued growth in 2025.

OPPO (including OnePlus and Realme) ranked fourth, falling slightly by 1.1% quarter-to-quarter to 36.8 million units in Q4/2024. Full-year 2024 production rose by 3.1% year-and-year to 143.4 million units. While OPPO also benefited from China’s subsidies, the impact was primarily seen in increased high-end smartphone sales rather than overall volume growth.

Vivo (including iQoo) ranked fifth, growing by 5.9% quarter-to-quarter to 28.6 million units in Q4/2024. Full-year 2024 production for 2024 grew by 10.2% year-on-year to 103 million units, with sales growth driven by China’s subsidy policies.

Transsion (including TECNO, Infinix, and itel) secured sixth place, growing by 5.9% quarter-to-quarter to 27 million units in Q4/2024. Full-year 2024 production reached 105.9 million units, largely fueled by aggressive inventory replenishment in Q1//2024. However, since Transsion’s primary markets are outside China, it did not benefit from Chinese subsidies, leading to weaker production growth in second-half 2024 compared with Vivo.