News: Markets

5 March 2025

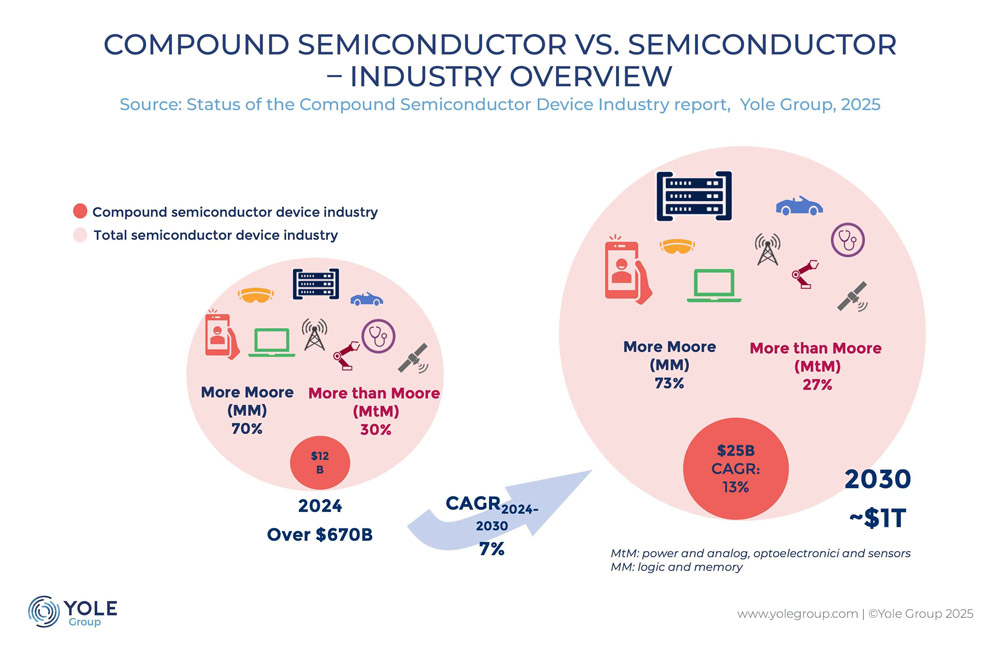

Compound semiconductor market growing at nearly 13% CAGR to $25bn by 2030

According to the new market & technology report ‘Status of the Compound Semiconductor Device Industry’ from market analyst firm Yole Group, the compound semiconductor device market is growing rapidly at a compound annual growth rate (CAGR) of nearly 13% from 2024 to about $25bn by 2030, outpacing the broader semiconductor market.

This remains a small part of the overall $1 trillion semiconductor device market, but compound semiconductors are enablers, driven by strong market dynamics, notes Yole. “This acceleration is fueled by the booming automotive and mobility sectors, with strong momentum also coming from telecom, infrastructure, and consumer electronics,” says Ezgi Dogmus PhD, activity manager, Compound Semiconductors at Yole Group.

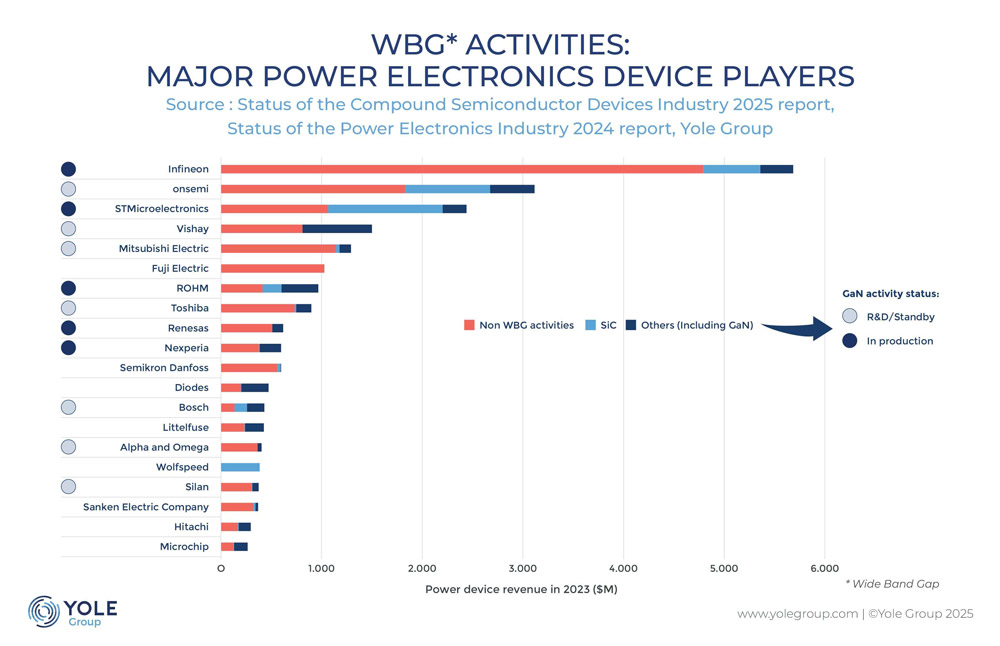

In this dynamic context, major semiconductor players are increasingly interested in compound technologies. Over the past decade, a rapid push for power silicon carbide (SiC) adoption saw Wolfspeed divest its RF and LED businesses to concentrate on SiC. In parallel, STMicroelectronics, onsemi and Infineon Technologies expanded their SiC investments, adopting vertically integrated business models to reduce wafer supply dependencies amid geopolitical tensions.

After SiC adoption, is GaN the next big breakthrough?

Following the SiC boom (forecasted to reach $10bn in 2029, according to Yole’s ‘Power SiC – Market and Applications report, 2024 edition’), original equipment manufacturer (OEMs) are showing stronger interest in GaN for power electronics applications. This interest has led to a change in the landscape. The power GaN market is projected to grow beyond $2bn by 2029, with a strong five-year CAGR, according to Yole Group’s ‘Power GaN 2024 report’.

As of 2025, Innoscience, Power Integrations and Navitas lead the power GaN market. In parallel, semiconductor companies Infineon Technologies and Renesas grew inorganically by acquiring GaN Systems and Transphorm, respectively.

“It has also created synergies with GaN for RF applications,” notes Poshun Chiu, senior technology & market analyst, Compound Semiconductors, at Yole Group. “Companies like Infineon Technologies and GlobalFoundries, having invested in power GaN-on-Si, are exploring synergies to leverage existing equipment, such as epitaxy, for RF production.”

RF applications: a unique perspective?

RF gallium arsenide (GaAs) was the first compound semiconductor to achieve success in consumer applications, with a well-established ecosystem by 2025. Skyworks leads the market, followed by Qorvo and Murata, securing design wins in consumer end systems. However, geopolitical restrictions are driving Chinese OEMs to develop a local ecosystem.

“RF GaN was initially adopted in defense applications like radar, but over the past decade it has expanded into telecom infrastructure, meeting 5G base-station requirements,” notes Aymen Ghorbel, technology & market analyst, Compound Semiconductors, at Yole Group. “Interest in satellite communications and other use cases has also grown.”

AI boom driving datacom growth and powering compound semiconductors

The photonics compound semiconductor industry is being driven by semiconductor lasers, the market for which is expected reach $5bn by 2029. These technologies are widely used in communication, sensing, and various other applications. With the rise of artificial intelligence (AI), the datacom sector has seen significant growth, driving strong demand for silicon photonics.

At Yole, analysts have identified a growing number of collaborations between the indium phosphide (InP) photonics and silicon industries. Major semiconductor giants like TSMC are entering the photonics business. And, step by step, more players, such as GlobalFoundries and Samsung, may follow in the future.

Micro-LED display, a fragmented landscape

The micro-LED display industry is highly fragmented, with no single entity overseeing manufacturing from start to finish. Unlike traditional vertically integrated display production, micro-LED manufacturing requires distinct expertise.

Major display makers like BOE and AUO are securing control over LED suppliers, while startups and equipment makers contribute to major technologies. Geographic alliances, particularly in China and Taiwan, are shaping industry dynamics. Apple’s withdrawal has slowed funding, leaving most startups struggling and undermining confidence in micro-LED’s prospects, Yole concludes.

Compound semiconductor substrate market growing at 17% CAGR to $3.3bn in 2029