News: Optoelectronics

14 May 2026

Lumentum’s quarterly revenue grows 90% year-on-year to $808.4m

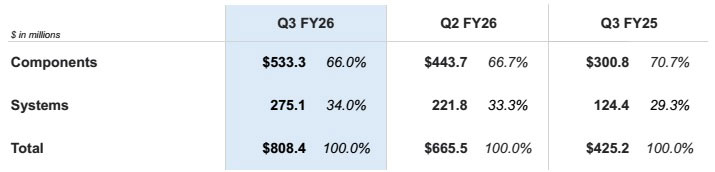

For its fiscal third-quarter 2026 (ended 28 March), Lumentum Holdings Inc of San Jose, CA, USA (which designs and makes photonics products for optical networks and lasers for industrial and consumer markets) has reported record revenue of $808.4m (above the midpoint of the $780–830m guidance range). This is up 21.5% on $665.5m last quarter and 90.1% on $425.2m a year ago, due primarily to growth in transceivers and laser chips for cloud and AI applications.

Component revenue grows 77.3% year-on-year

Components segment revenue was $533.3m (66% of total revenue), up 20.2% on $443.7m last quarter and 77.3% on $300.8m a year ago. Shipments of narrow-linewidth laser assemblies for data-center interconnects (DCI) grew for the ninth consecutive quarter, rising over 120% year-on-year. Shipments of pump lasers for scale-across and sub-sea applications grew by 80% year-on-year.

“These components [narrow-linewidth laser assemblies and pump lasers] remain effectively sold out for the foreseeable future, and we are actively working to secure long-term agreements that will help offset anticipated capital expenditures,” says president & CEO Michael E. Hurlston.

Regarding laser chips: “We achieved another quarterly company record in EML [electro-absorption modulated laser] shipments (with unit shipments more than doubling year-on-year), led by 100G lane speeds. 200G EML revenue more than doubled sequentially,” says Hurlston. “Our ultra-high-power laser chip manufacturing ramp for CPO [co-packaged optics] applications is also proceeding according to plan… We achieved sequential growth,” he adds.

“We continue to ship CW lasers to 800G transceiver manufacturers, and starting in fiscal Q3 we began supplying CW lasers for internal use in our cloud transceiver business,” says Hurlston.

Systems revenue grows 121% year-on-year

Systems segment revenue was $275.1m (34% of total revenue), up 24% on $221.8m last quarter and 121% on $124.4m a year ago, driven mainly by record shipments of cloud transceivers (up more than 40% sequentially) as the firm leverages its expanded manufacturing footprint in Thailand.

Industrial lasers were approximately flat sequentially, while cable access shipments remain muted, declining quarter-on-quarter due to customer and timing factors.

Margins and income exceed guidance

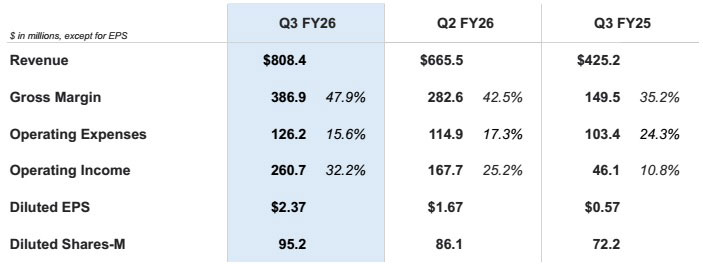

On a non-GAAP basis, gross margin has grown further, from 35.2% a year ago and 42.5% last quarter to 47.9%. This resulted from improved manufacturing utilization across most product lines, increased pricing on select products, and favorable product mix (driven primarily by growth in data-center laser chips).

“Mix was aided by strength in [data-center] laser chips, but also by a less-heralded part of our portfolio, ‘scale-across’ components, which include our pump lasers and narrow-linewidth laser assemblies,” says Hurlston.

R&D expenses have risen from $63.3m a year ago and $69.9m last quarter to $78.4m. “While continuing to invest in critical R&D programs serving cloud and AI customers, we have maintained the rigorous cost controls necessary to optimize our business model,” says executive VP & chief financial officer Wajid Ali. Selling, general & administrative (SG&A) expenses have risen less, from $40.1m a year ago and $45m last quarter to $47.8m.

While operating expenses have risen from $103.4m a year ago and $114.9m last quarter to $126.2m in support of expanding cloud opportunities, this is a cut from 24.3% of revenue a year ago then 17.3% last quarter to just 15.6%.

Driven primarily by revenue growth in components products (fueled by a rich product mix and strong operating leverage), operating income has grown further, from $46.1m (operating margin of 10.8%) a year ago and $167.7m (25.2% margin) last quarter to $260.7m (32.2% margin, above the expected 30–31% range).

Likewise, net income has risen further, from $40.9m ($0.57 per diluted share) a year ago and $143.9m ($1.67 per diluted share) last quarter to $225.7m ($2.37 per diluted share, above the expected $2.15–2.35 range).

Capital expenditure (CapEx) was $125m, focused mainly on expanding manufacturing capacity to support cloud and AI customers.

During the quarter, cash, cash equivalents, and short-term investments rose by $2017m, from $1155.3m to $3172.3m. This was due mainly to the proceeds from the issuance of Series A convertible preferred stock in March, with NVIDIA making a direct investment of $2bn.

To support the anticipated growth in cloud and AI-related revenue streams, inventories has been increased by a further $62m sequentially, from $570.4m to $632.8m (following a $39m boost last quarter).

Demand exceeding production capacity, leading to undershipping

For fiscal fourth-quarter 2026 (ending 27 June), Lumentum expects revenue to grow to a new record of $960–1010m. Operating margin is expected to rise to 35–36%. Diluted earnings per share should rise to $2.85–3.05.

Over half of the sequential revenue growth will stem from components business. The remainder will be driven by the continued ramp of the systems portfolio, primarily through high-speed transceivers and additional contributions from OCS.

“Our current numbers and guidance reflect continued success in EML lasers [with unit shipments on track to grow by more than 50% from December-quarter 2025 to December-quarter 2026] and our scale-across components,” says Hurlston. “We are seeing improved performance in our cloud modules business, which has grown significantly across the last few quarters. In addition, while we’re seeing initial contributions from both scale-out CPO and OCS, they are still relatively modest. Furthermore, our largest single growth driver, scale-up CPO, is still very much in its infancy,” he adds. “As our key growth drivers of co-packaged optics [CPO] and optical circuit switches [OCS] begin to kick in, we would expect further increases in earnings power.”

“Ultra-high-power laser chips for CPO applications… are on schedule to both deliver meaningful revenue in our December quarter and fulfill the multi-hundred-million-dollar purchase order slated for the first half of calendar year 2027,” notes Hurlston. “In addition, our development work continues with multiple CPO customers through collaborations that leverage our laser chip technologies within a pluggable turnkey ELS [external laser source] module solution,” he adds.

“We are poised to ramp 1.6T-speed transceiver shipments in fiscal Q4, with a portion of this volume leveraging our own CW lasers,” says Hurlston. Internal CW laser production is expected to contribute to about 20% of transceivers, with anticipated margin benefit as insourcing volumes increase. Margins for 1.6T transceivers are better than those for 800G transceivers. However, overall transceiver segment margin is “still a bit challenged”. “We are improving transceiver profitability through better yields and lower scrap rates. Despite these gains, supply constraints on critical components keep our shipments well below customer demand,” he adds.

“In OCS, the multi-year, multi-billion-dollar purchase agreement we recently announced ensures sustained long-term growth. Our OCS ramp is largely on track, although our pace and slope are gated by the supply chain. We are experiencing considerable tightness in this product area due largely to the significant step-up in requested output. On the other hand, the number of new opportunities we are seeing for optical switches is putting tension on our roadmap, and we are having to make choices across the company in order to service them.”

“Our wafer fab capacity in Japan remains at a premium and is fully allocated to meet surging customer demand,” notes Hurlston. “We are significantly under-shipping demand... We’re having to make choices as to who we support. We’re trying to be as fair and reasonable as possible, but we are having to make choices as to how we allocate our [laser] pump demand.”

To provide the capacity needed for future growth, in mid-March Lumentum announced its acquisition from RF & power device maker Qorvo Inc of a fab in Greensboro, North Carolina, which is now being converted from gallium arsenide (GaAs) to become Lumentum’s fifth indium phosphide fab. “We expect to take advantage of a significant number of the tools that already exist in our Greensboro site,” says Hurlston. Revenue contribution is expected to begin six or so quarter from now.

“We are very much on track to reach our $2bn quarterly revenue goal,” believes Hurlston.

Lumentum joining Nasdaq-100 Index on 18 May

Lumentum to establish new US plant to manufacture indium phosphide lasers for AI data centers

NVIDIA announces strategic partnership with Lumentum to develop data-center optics

Lumentum’s quarterly revenue grows 65% year-on-year to $665.5m