News: LEDs

29 October 2020

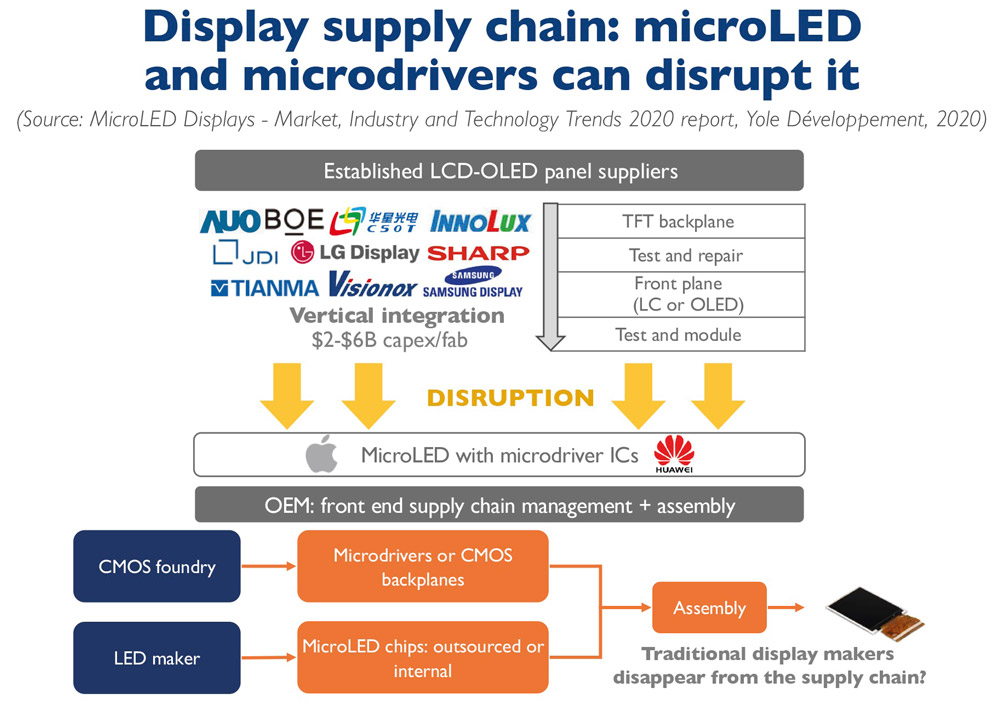

Apple’s micro-LED supply chain to disrupt display industry?

Over $5bn has already been spent on micro-LED development (as of first-quarter 2020), estimates Yole Développement in its report ‘MicroLED Displays - Market, Industry and Technology Trends 2020’. Despite the global COVID-19 pandemic, money is still flowing into the micro-LED ecosystem, with the impact on the global industry varying according to the application.

“For many companies, interest in micro-LEDs lies beyond just the ability to offer the latest display technology,” asserts Eric Virey PhD, Yole’s principal analyst, Technology & Market, Displays. “Intellectual property (IP) analyses indicate that Apple is planning to forgo TFT (thin-film transistor) backplanes, instead opting for silicon CMOS micro-drivers,” he adds. “The implications go far beyond a technological choice. Apple’s micro-LED supply chain would eliminate reliance on display makers such as Samsung or LG”.

Apple can source micro-drivers and micro-LED chips from foundry partners and assemble those components in-house or with other partners to create unique displays. Although it currently has more pressing battles to fight, the same logic applies to Huawei, with the possible added benefits of a 100% domestic display supply chain that does not rely on restricted US technology.

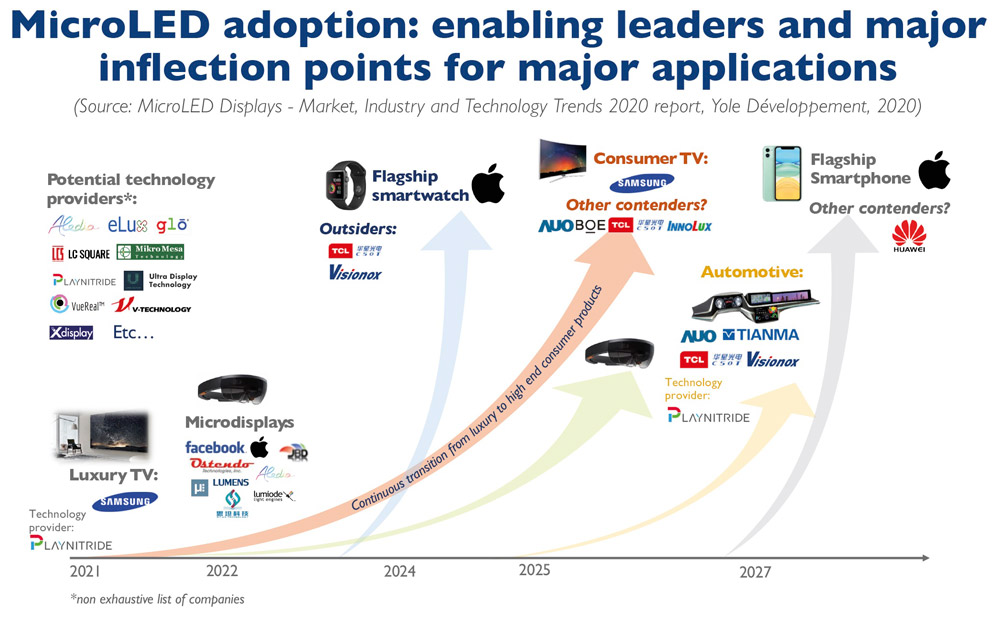

The key players and inflexion points vary from one application to another. Apple will lead on smartwatch applications and Samsung on TVs, which will evolve smoothly from luxury products in excess of $100,000 towards high-end consumer devices, expects Yole.

For Samsung’s TV division Samsung Visual Display (SVD), micro-LEDs would confer the ability for it to compete against organic light-emitting diodes (OLEDs) in the high-end, large TV segment with a technology that does not rely on panels from China or its friendly enemy Samsung Display Co Ltd (SDC). SVD’s micro-LED technology still uses LTPS (low-temperature polysilicon) TFTs but, thanks to its modular design, only requires smartphone-sized tiles that could be sourced from existing G6 fabs.

Other display makers such as BOE or CSOT want to leverage their existing TFT infrastructure. Samsung Display is developing QNEDs, its own flavor of micro-LEDs that could fast track the technology and leverage most of its quantum dot (QD)-OLED investments.

For AUO, micro-LEDs could be a matter of survival. The firm has been successfully managing cash by limiting capital expenditure (CapEx) and focusing on high-added-value products. But China won the LCD war and the company never significantly invested in OLED capacity, making it difficult to pursue this strategy in the long term. Micro-LEDs represent AUO’s best shot at remaining relevant in high-end automotive and TV panels, without requiring the massive CapEx of an OLED fab. The firm has already shown various automotive prototypes and could demonstrate TV prototypes in 2021.

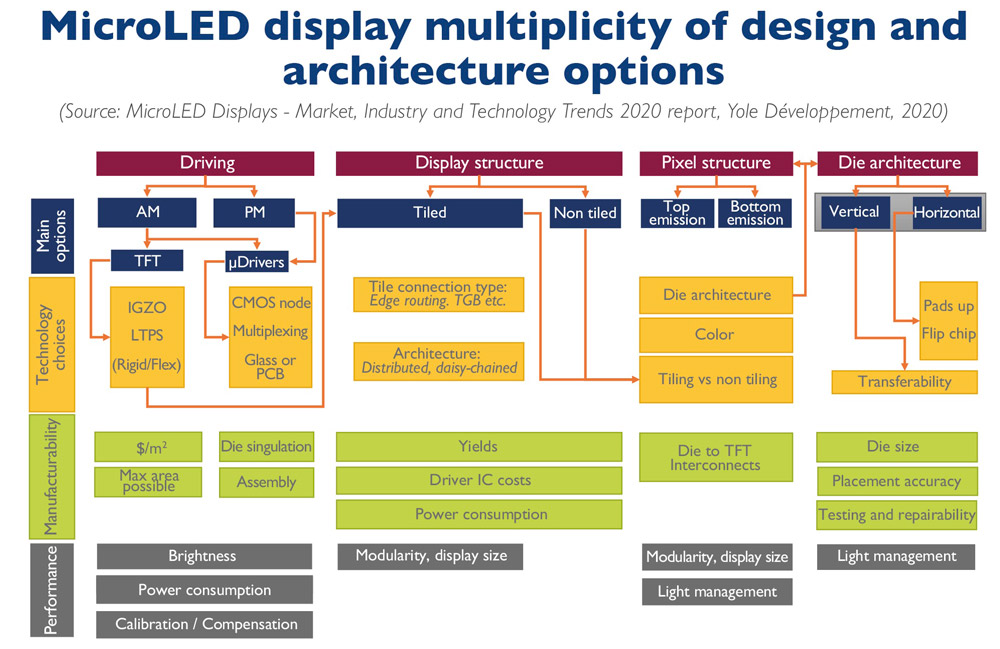

The availability of standard tools and processes enabled the commoditization of LCDs and will soon do so for flexible red/green/blue (RGB) OLEDs. Despite significant progress in micro-LED technology, however, roadblocks remain, including power efficiency, transfer and assembly, yield management, driving. The challenges lie in the yield, manufacturability and cost effectiveness of those solutions.

The lack of micro-LED process maturity and the proliferation of technology paths hinders the development of high-volume manufacturing tools and the development of the supply chain. However, this complexity is a welcome barrier to entry for companies such as Apple or Samsung. Both have the financial and technological strength to develop end-to-end solutions internally and acquire missing technology building blocks as needed.

Latecomers or smaller companies are eager to see micro-LED processes converge and off-the-shelf tools become available. Equipment makers such as Toray Engineering, TDK, V-Technology, Besi, SET and others are making the first attempts, while technology providers such as Playnitride, XDC and many others can license key processes and components.

For high-volume consumer applications, economics are driving die size to below 5µm, with stringent yield requirements for which traditional LED fabs are not suited. A paradigm shift is required towards a semiconductor-like manufacturing mindset with high efficiency, automation, end-to-end defect prevention and management strategies, says Yole.

This is creating an additional push toward the adoption of larger-diameter substrates. Going from 6” to 8” is especially desirable, as it grants access to battle-tested, retrofitted semiconductor equipment. This also increases the appeal for gallium nitride on silicon (GaN-on-Si) platforms that are readily available in 8” and already looking toward 12”. Although they are more challenging, 8” sapphire and gallium arsenide (GaAs) platforms however remain credible options.

Micro-LED technologies make significant progress over last 18 months