News: Markets

14 July 2022

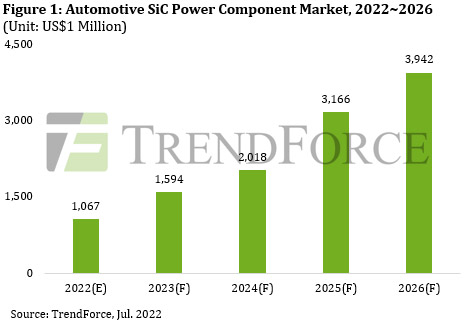

Automotive SiC power component market to grow to $1bn in 2022 then $3.94bn by 2026

To further improve the power performance of electric vehicles (EV), major global automakers have focused on a new generation of silicon carbide (SiC) power components and have successively launched a number of high-performance car models equipped with corresponding products. According to research by TrendForce, as more and more auto-makers begin to introduce SiC technology into electric drive systems, the market for vehicle SiC power components is forecast to grow to $1.07bn in 2022 then $3.94bn by 2026.

The automotive SiC power component market is currently dominated by major European and American IDMs, notes TrendForce. The key suppliers STM, onsemi, Wolfspeed, Infineon and ROHM have long been deeply involved in this field and have close interactions with major auto-makers and tier-1 manufacturers. The affluence of the automotive market has also impressed the importance of stable supply capacity onto major manufacturers. Therefore, in an effort to exert full control on the supply chain, they have moved successively into the upstream substrate materials field. For example, onsemi acquired GT Advanced Technologies last year.

Major auto-makers have high hopes for SiC and are simultaneously and vigorously participating in the construction of supply chains. From the perspective of China (the world’s largest EV market), auto-makers such as SAIC and GAC have begun to deploy an entire SiC industry chain, which has created invaluable development opportunities for domestic suppliers. At the same time, auto-makers such as BYD and Hyundai have launched their own chip R&D programs, which have injected new vitality into the market.

In addition, the cost-effectiveness of using SiC power components has always been a market concern and its key lies in upstream substrate materials. The industry is experimenting with various methods to further reduce costs, including new crystal growth approaches (UJ-Crystal, Jing Ge Ling Yu), high-efficiency wafer processing technology (Soitec, Disco, Infineon, Lasic Semiconductor Technology), and following Wolfspeed in migrating from 6-inch to 8-inch wafer technology.

With continuing breakthroughs in SiC materials technology and the maturity of chip structure and module packaging processes, the penetration rate of SiC power components into the automotive market is expected to maintain an upward trajectory and will gradually extend from existing high-end vehicle applications to medium- and low-end vehicles in order to accelerate the process of vehicle electrification, concludes TrendForce.

Annual 6-inch SiC wafer demand for EVs to reach 1.69 million units in 2025