News: Suppliers

24 August 2022

Veeco grows revenue 4.9% in Q2, despite supply chain constraints

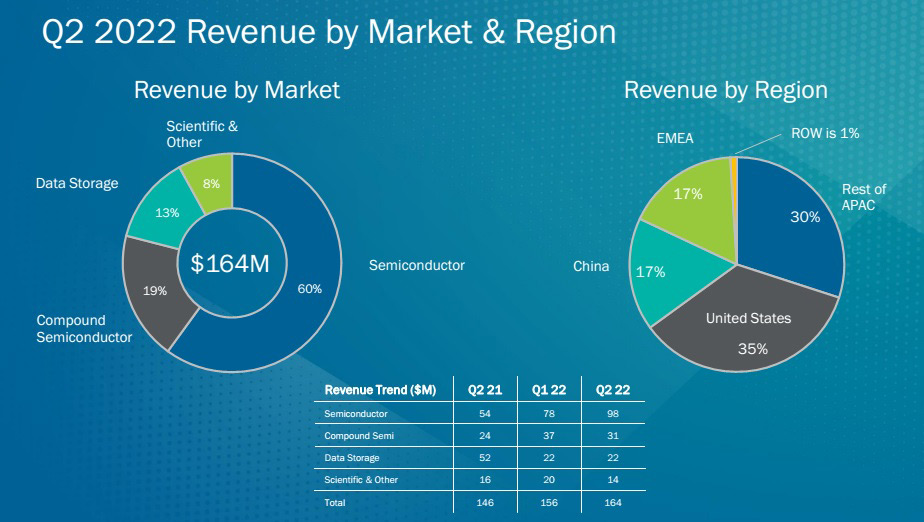

For second-quarter 2022, epitaxial deposition and process equipment maker Veeco Instruments Inc of Plainview, NY, USA has reported revenue of $164m (above the midpoint of its $150-170m guidance). This is up 4.9% on $156.4m last quarter and 12% on $146.3m a year ago, despite revenue being impacted by some demand not being able to be fulfilled due to supply chain constraints.

Growth was driven by the Semiconductor sector (Front-End and Back-End, as well as EUV Mask Blank systems and Advanced Packaging) reaching another record of $97.5m (59.5% of total revenue). This is up 25.6% on $77.6m last quarter and 81.6% on $53.7m a year ago, due to significant contributions from laser annealing and advanced packaging lithography systems. “Demand is stemming predominantly from advanced- and trailing-node logic applications [artificial intelligence (AI) and high-performance computing (HPC), as well as mature automotive and consumer applications], where Veeco’s semiconductor exposure is greatest,” notes CEO Bill Miller.

The Compound Semiconductor sector (Power Electronics, RF Filter & Device applications, and Photonics including specialty, mini- and micro-LEDs, VCSELs, laser diodes) contributed $31.1m (19% of total revenue). This is down 16.2% from $37.1m last quarter (due to a slowdown in 5G RF-related activity) but up 28.5% on $24.2m a year ago (driven by systems shipments for photonics applications). “We shipped multiple deposition systems to support laser diodes for optical communication and specialty LED production,” notes Miller.

Data Storage contributed $21.5m (13.1% of total revenue), more than halving from $52m a year ago but roughly level with $21.6m last quarter.

The Scientific & Other segment contributed $13.8m (8.4% of total revenue), down 31.3% on $20.1m last quarter and 15.9% on $16.4m a year ago.

By region, the USA comprised 35% of total revenue (driven primarily by sales of laser annealing and advanced packaging lithography systems). The Asia-Pacific region (excluding China) comprised 30% (driven mainly by Semiconductor system sales). Europe, Middle-East & Africa (EMEA) comprised 17% of total revenue. China comprised 17% of total revenue (primarily for photonics applications).

On a non-GAAP basis, gross margin was 40.3%, down from 43.1% last quarter and 41.6% a year ago. This was due to an unfavorable product mix (since two of the three evaluation tools that were signed-during the quarter were offered with especially low pricing). “We expect gross margins to improve in the second half compared to Q2,” notes chief financial officer John Kiernan.

Operating expenses have risen further, from $39.6m a year ago and $42.8m last quarter to $43.2m, although this is below the expected $44-46m.

Operating income was $23m, down from $24.7m last quarter but up on $21.3m a year ago (and exceeding the guidance of $15-22m).

Net income was $20m ($0.35 per diluted share), down from $21.7m ($0.38 per diluted share) last quarter but up from $17.9m ($0.35 per diluted share) a year ago, and exceeding the guidance of $12-19m ($0.22-0.34 per diluted share).

Cash flow from operations was $3.4m. Capital expenditure (CapEx) was $4.5m. During the quarter, cash and short-term investments hence fell only slightly, from $232m to $231m. Long-term debt, including the current portion of $20m, was recorded at $274m on the balance sheet and represents the carrying value about $278m in convertible notes.

“We’re experiencing success with the investments we’ve made in our evaluation program, as demonstrated by the continued adoption of our technologies by leading customers,” says Miller.

“We’re working to penetrate the compound semiconductor market with our MOCVD solutions by targeting micro-LED and power electronics applications. Our gallium nitride and arsenide-phosphide systems are in the field under evaluation with leading customers,” he adds.

“In the power electronics case, we’re working with a foundry customer who is evaluating our Propel single-wafer gallium nitride system for 8-inch power applications. We believe there are opportunities in the consumer, automotive and data-center power markets to enable improved cost of ownership.”

“In micro-LED, we’re engaged in two applications working with a number of leaders in the industry for five-plus years. The first approach is more traditional, where red, green and blue micro-LEDs are produced independently and transferred to a display. We have our aluminium arsenide phosphide system under evaluation for red micro-LED opportunities. We expect this evaluation to close in the second half of this year. For the second approach, we have 200mm and 300mm gallium nitride systems that we’re deploying for an innovative micro-LED application where the blue, green and red pixels are produced on the same silicon wafer. Both approaches can potentially be a good long-term opportunity for the company going forward,” believes Miller.

“While our demand is quite strong, we’ve not seen a meaningful improvement in inbound material lead times,” notes Kiernan. In this constrained supply chain environment, for third-quarter 2022 Veeco expects revenue of $160-180m. Due to a more favorable product mix than in Q2, gross margin should improve to 41-43%. With operating expenses of $45-47m, operating income should be $21-30m and net income $18-28m ($0.32-0.48 per diluted share).

With healthy order activity (especially in the Semiconductor and Data Storage markets), demand for Veeco’s products continues to outpace supply, leading to growing order backlog, notes Veeco.

“Our San Jose facility ramp is on schedule, and our operations will be fully transferred to the new building by the end of Q3,” says Miller. “The increased manufacturing footprint is enabling the ramp of our laser annealing output to meet our customers demand. Demand for laser annealing remains healthy as we see customers adopt our technology and add capacity, because our laser annealing platform is a production tool of record at the world’s leading logic players,” he adds. “Beyond Q3/2022, although supply-chain challenges persist, we continue to experience strong demand for our products,” says Kiernan. “We’re reiterating our previously guided full-year revenue range of $640-680m and diluted non-GAAP EPS range of $1.50-1.70 per share.” By market segment, Veeco expects year-on-year revenue growth of 50% in Semiconductors (to about $370m), 20-25% in Compound Semiconductors (to $130m), and 10% in Scientific & Other (to $70m, or just over 10% of total revenue). Data storage is expected to fall by about 45% (to $90m).

“We are excited to introduce laser annealing to the memory market,” states Miller. “In fact, a leading DRAM manufacturer recently signed-off their evaluation system for a future node. We anticipate follow-on orders in the late 2023 or early 2024 timeframe to support our customers manufacturing plans. Overall, our laser annealing business is growing as we win process steps and new customers,” he concludes.

Taiwan Semiconductor Research Institute selects Veeco’s Propel MOCVD system

Veeco grows revenue 28% in 2021

Veeco’s Q3 revenue up 34% year-on-year to $150m

Veeco’s Q2 revenue up a more-than-expected 48% year-on-year to $146.3m