News: Suppliers

13 November 2020

Veeco’s revenue grows 14% in Q3

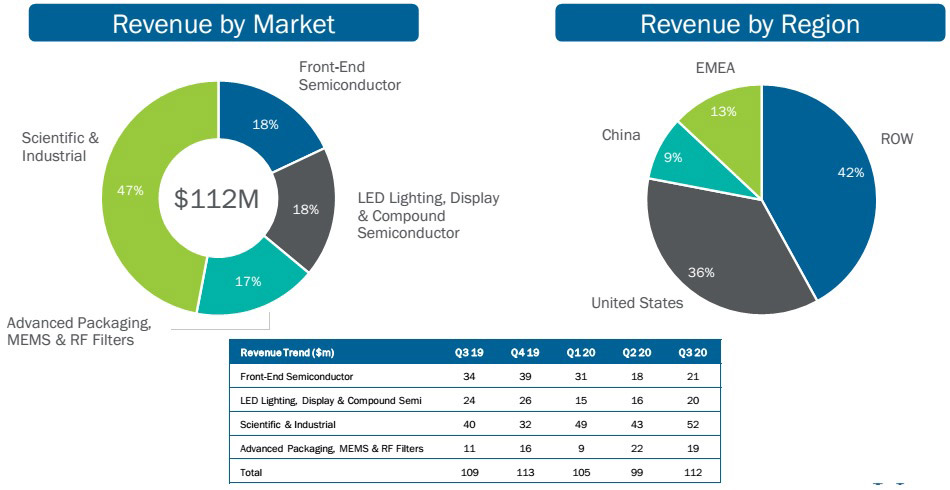

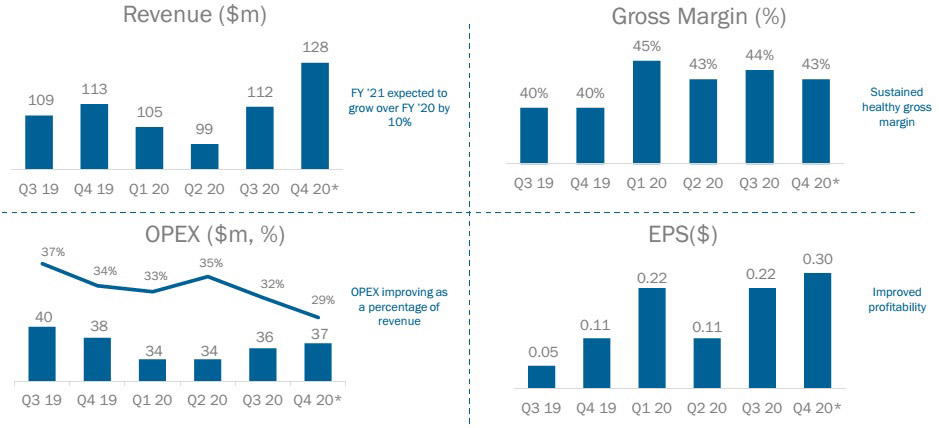

For third-quarter 2020, epitaxial deposition and process equipment maker Veeco Instruments Inc of Plainview, NY, USA has reported revenue of $112.1m, up 14% on $98.6m last quarter and 2.8% on $109m a year ago (and above the midpoint of the $100-120m guidance).

“While maintaining all health and safety measures [during the COVID-19 pandemic], we continue to operate at normal capacity,” notes CEO Bill Miller.

The Scientific & Industrial segment comprised 47% of total revenue (rising from 44% last quarter), led by ion beam system shipments to data-storage customers. “There has been significant activity in our data-storage market related to data-center and Cloud storage demand,” says Miller.

“We’re also seeing significant customer engagement in advanced-node semiconductor manufacturing, 5G RF and power electronics,” he adds.

The Front-End Semiconductor segment (formerly part of the Scientific & Industrial segment, before the 2017 acquisition of lithography, laser-processing and inspection system maker Ultratech) again contributed 18% of total revenue, driven by an ion beam deposition system shipped for making extreme ultraviolet (EUV) mask blanks. “We were encouraged by our laser annealing customer activity in the quarter [foundries and integrated device manufacturers] and expect laser annealing to become a bigger revenue contributor in the upcoming quarters,” says Miller.

The Advanced Packaging, MEMS & RF filter segment – including lithography and Precision Surface Processing (PSP) systems sold to integrated device manufacturers (IDMs) and outsourced assembly & test firms (OSATs) for Advanced Packaging in automotive, memory and other areas – comprised 17% of total revenue (falling back from 22% last quarter), with a shift of systems into 5G RF filter and advanced packaging applications.

The LED Lighting, Display & Compound Semiconductor segment – which includes photonics, 5G RF, power devices and advanced display applications – comprised 18% of total revenue (up from 16% last quarter), driven by a broad number of applications for metal-organic chemical vapor deposition (MOCVD) systems including RF & power devices, as well as advanced applications in photonics.

By region, the rest of the world (which includes Japan, Taiwan, Korea and South-east Asia) comprised 42% of revenue (rebounding from 26% last quarter), driven by sales of ion beam deposition systems to EUV mask blanks plus data-storage customers in South-east Asia. The USA rebounded from 30% to 36% of revenue, including sales of systems for data storage as well as advanced packaging and power electronics. Europe, the Middle East & Africa (EMEA) was 13% of revenue, comprising mainly sales to compound semiconductor customers. China shrank from 18% to 9% of revenue, as expected, since the regulatory environment is providing headwinds.

“MOCVD is at historically low revenue levels right now, driven by the fact that we decided to exit the commoditized China blue LED business. So over the last year and a half or so, we did a lot of work restructuring the business, and really focusing on new markets and new opportunities,” notes Miller. “We’re starting to gain some traction with the Propel system and for power & 5G RF with [South Korea-based] A-Pro Semicon,” he notes.

On a non-GAAP basis, gross margin has risen further, from 40.3% a year ago and 43% last quarter to 44.5%, exceeding the 42-44% guidance range.

Operating expenditure (OpEx) was $35.7m, up from $34.4m last quarter but cut from $40m a year ago, and falling further from 37% of revenue a year ago and 35% last quarter to just 32%.

“We are pleased with our advancing profitability in the quarter, which was driven by our ion beam technologies sold into the Data Storage market,” says Miller.

Operating income has risen from $4m a year ago and $8m last quarter to $14.1m. “Our non-GAAP operating income improved significantly year-on-year [by $10m, despite revenue being similar], demonstrating the early effectiveness of our transformation,” says Miller. “Our sustained profitability is a result of the work we completed over several quarters to improve our operating model, such as expanding gross margins, and restructuring to reduce costs.”

Likewise, net income has risen further, from $2.6m ($0.05 per diluted share) a year ago and doubling from $5.5m ($0.11 per diluted share) last quarter to $11m ($0.22 per diluted share), towards the top of the $5-12m ($0.10-0.26 per diluted share) guidance range.

Cash flow from operations was $10m. Capital expenditure (CapEx) was $1.4m. During the quarter, cash and short-term investments rose by $9m, from $301m to $310m.

Long-term debt on the balance sheet has risen from $317m to $321m, representing the carrying value of $382m in convertible notes.

From a working capital perspective, accounts receivable rose from $67m to $80m (as the firm increased shipments). Days sales outstanding (DSOs) rose slightly from 61 to 64 days. This was partially offset by accounts payable rising from $26m to $34m, driving up days payable outstanding (DPO) from 42 to 49 days. Inventory rose from $137m to $143m, resulting from investments made to increase shipments and provide evaluation systems to customers in support of Veeco’s growth strategy in semiconductor and compound semiconductor markets.

“We have strong customer engagements… Entering the fourth quarter, we’re in a strong backlog position,” says Miller.

“In compound semiconductor markets, our MOCVD product is well positioned to address applications like power electronics, 5G RF, VCSELs [vertical-cavity surface-emitting lasers] and edge-emitting lasers and micro-LEDs,” believes Miller. “We’re experiencing an uptick in demand for MOCVD systems, certainly in the third quarter from order activity. We received multiple orders for high-volume Propel systems for power electronics, RF devices and early-stage micro-LED applications,” he adds.

“What we’re seeing now is the introduction of GaN power devices in consumer electronic products. For applications like fast charging, wireless charging is driving demand,” says Miller. “There are also other customers trying to qualify GaN in the automotive market, not in the high-power silicon carbide (SiC) high-voltage areas [for electric vehicles] but for power management throughout automotive. Our product, the Propel single-wafer tool is pretty well positioned there,” he believes.

“A-Pro Semicon based in Korea has selected Veeco’s Propel HVM MOCVD system for GaN-based power and 5G RF semiconductor device manufacturing. Our single-wafer gallium nitride Propel system has been well received by leading customers for its proven high-performance capability,” Miller continues.

“Aledia, a developer of next-generation advanced displays, has selected Veeco’s Propel 300mm MOCVD system to manufacture 3D nanowire micro-LED displays. The system features a SEMI-compliant equipment front-end module with full automation and was chosen due to its excellent productivity and film quality,” he adds.

“Osram Opto Semiconductors qualified our Lumina arsenide-phosphide MOCVD beta system to drive their next generation of advanced photonic devices. The performance Osram demonstrated reinforces our confidence in Lumina’s capability. Also, we have an evaluation agreement in place with another leading customer [a beta system for micro-LED applications] which will further advance our ability to drive long-term growth.”

“Given our visibility, we expect continued strength in our overall business and feel confident about our future performance,” says Miller.

For fourth-quarter 2020, Veeco expects revenue to grow to $120-136m. Gross margin should be flat to down, at 42-44%, reflecting additional service expenses to support customer evaluations. Operating income is expected to be $14-22m. Net income should be $11-19m ($0.22-0.37 per share), despite OpEx being flat to up, to $36-38m. “On a go forward basis, we expect to keep SG&A close to current levels, but are making strategic investments in R&D to support our growth initiatives,” says chief financial officer John Kiernan.

“We will have a strong finish to 2020 and are optimistic about 2021,” believes Miller. “Based on our current visibility and forecasted backlog, we expect revenue growth in full-year 2021 in the 10% range compared with full-year 2020,” adds Kiernan.

“We’re confident in our execution in the near-term based upon multiple customer engagements where the pull for production solutions is strong. This near-term growth stems from multiple product lines, and comes from the data-storage market, renewed demand in RF filters related to 5G, and continued activity in the front-end semiconductor market,” says Miller.

“With the first phase of our transformation behind us, we’ll continue to focus solidly on the second phase of our transformation, growing the company organically in the semiconductor and compound semiconductor markets,” says Miller. “Consistent with our longer-term strategy for growing in semiconductor and compound semiconductor markets, we’re making investments to solve our customers’ most difficult challenges with our core technologies,” he adds. “These investments include increased R&D and service spending, as well as inventory supporting evaluation tools at customer sites: evaluation agreements are in process for laser annealing systems for logic and memory applications, and MOCVD systems for early-stage micro-LED applications. This activity in high-value markets will be the catalyst for our growth in 2022 and beyond.”

Veeco retiring $125m of 2.70% convertible senior notes due 2023

Veeco’s Propel HVM MOCVD platform chosen by Korea’s A-Pro

Veeco returns to positive operating cash flow as it completes restructuring

Veeco’s Q1 revenue at high end of revised guidance range

Veeco’s revenue rebounds in Q4, as cost cutting yields a second quarter of profit

Veeco launches Lumina As/P MOCVD platform

Veeco’s revenue rebounds in Q3 as 300mm GaN MOCVD cluster system accepted for pilot production